Axel Merk discusses the relatively constant Gold to Asset ratio at the ECB (15%) in his latest Merk Insight letter and tries to analyze if this is done on purpose.

Here's the full letter:

When the euro was launched, the European Central Bank (ECB) held

approximately 15% of its assets in gold. That ratio has remained

reasonably stable, giving rise to a variety of chatter, including

suggestions that it may displace the U.S. dollar. We pursue the question

on whether the ECB’s gold holdings are an accident or strategy.

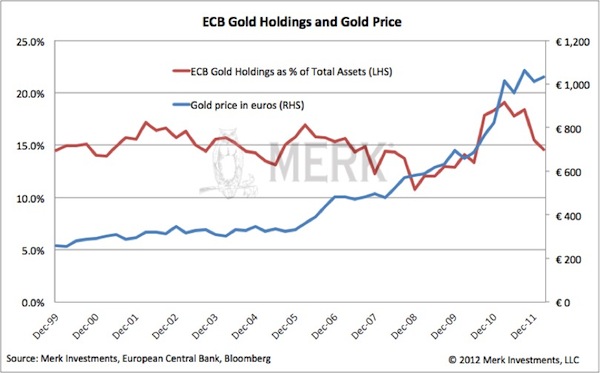

Let’s look at the numbers. Below is a chart depicting the

percentage of gold relative to the ECB’s total assets. As one can see,

the percentage has remained reasonably stable despite a significant

growth in total assets.

|

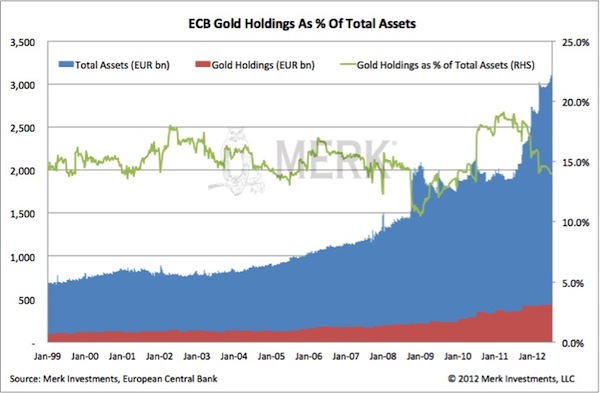

Total assets of a central bank may be considered a proxy

for the amount of money that has been “printed”; it’s a crude measure as

it does not reflect physical money printed; nor does it reflect money

in circulation; neither does it reflect sterilization activities that

also show a rise in assets. Still, a central bank balance sheet is often

referred to as the printing press as money is literally created out of

thin air (by the stroke of a keyboard) when assets are purchased.

Federal Reserve (Fed) Chairman Bernanke has referred to this fiat money

feature as the printing press. We like to think of it as super-money, as

central bank purchases provide cash to the banking system, allowing

them to lend a multiple of the money that has been “printed”. While

banks have been reluctant to lend (the velocity of money has been low),

the analogy we like to give is that if you give a baby a gun, just

because no one gets hurt does not mean it is not dangerous. That said,

let’s look at total assets at the ECB:

|

The interpretation shows that while money can be printed,

wealth cannot be created out of thin air: as money is printed, gold has

appreciated versus the euro. So while inflation has not shown up in

indicators such as the Consumer Price Index, monetary easing is

rightfully reflected in the price of gold.

Diving a little deeper to determine how much of

this is strategy versus accident, let’s look at the gold holdings at

the ECB once more:

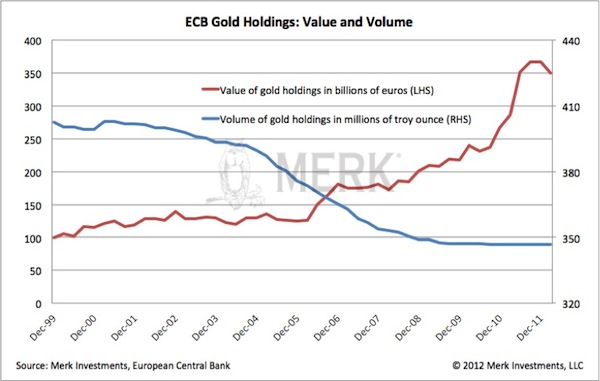

The ECB marks its gold holdings to market, i.e. uses

market prices for gold. The ECB was selling gold from the inception of

the euro until the onset of the financial crisis; since then, the ECB’s

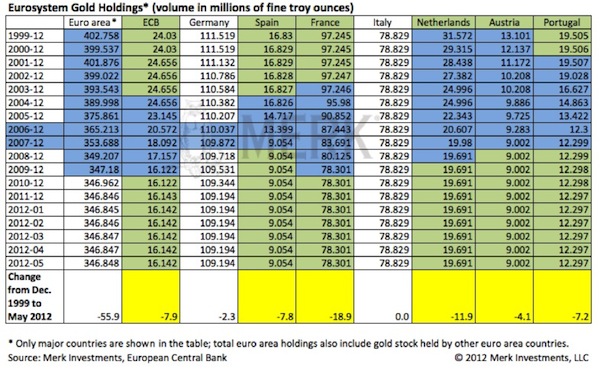

gold holdings have remained stable. To understand the motivation, one

needs to note that when one refers to ECB gold holdings, one is actually

talking about Euro area gold holdings. While the ECB holds some gold,

most gold is held by the respective central banks (this is not a

discussion of where such gold is physically located):

|

Relevant is that each nation in the Eurozone pursues

its own agenda with regard to its gold holdings. Germany has resisted

political pressure within Germany to sell gold, as Bundesbank (Buba)

profits would need to be transferred to the government; the hawkish Buba

has indicated that it would be considered selling gold to help finance

the government’s deficit. Italy, as one can see, has not sold any gold.

Conversely, as a percentage of their holdings, the Netherlands had been

rather eager to sell gold up until the financial crisis; Portugal, too,

was an aggressive seller. As one can see, gold sales are not

particularly related to the financial health of a Eurozone nation, but

more to the cultural attitude in the respective nations towards gold.

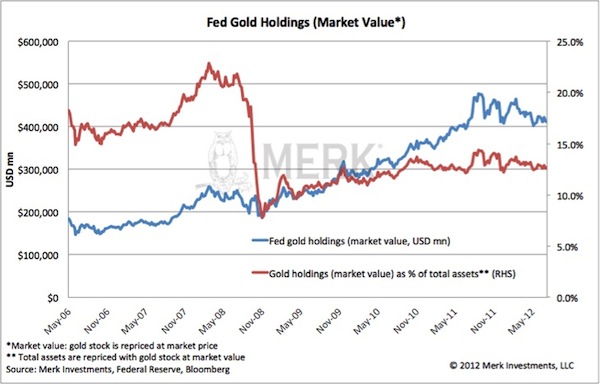

Let’s cross the Atlantic to see whether the ECB’s gold strategy is undermining the U.S. dollar. The Fed’s gold stock is valued at $44.22 per fine troy ounce. For purposes of the chart below, we adjust the Fed’s gold holdings to market prices:

|

Note that the chart above starts in 2006, so as to

focus on the period of the financial crisis. The Fed has been more

aggressive than the ECB in printing money. As such, the percentage of

gold in relation to total holdings has declined at the Fed in a more

pronounced fashion. There is clearly no perfect relationship between the

size of the balance sheet and the price of gold, as other factors also

influence the supply and demand of gold; however, increasing the supply

of fiat money (dollar, euros) may decrease its value when measured in

real assets, such as gold. We have in the past referred to the Fed as

the champ in printing money (as measured by the percentage balance sheet

growth since August 2008), although the Bank of England has, as of

late, taken on that title. But we digress.

From what we see, central banks have been scared into

holding gold since the onset of the financial crisis. Beyond that, we

don’t see an active strategy at the ECB to keep its gold reserves at 15%

of total assets. Instead, the ECB’s comparatively measured approach has

simply lead to a reasonably stable percentage of gold reserves. Of

course that was before ECB President Draghi said on July 26, 2012, that

he shall do “whatever it takes to preserve the euro.” (an interpretation

of that may be that more money printing is on the way). For now, the

cultural differences in responding to the financial crisis (Europe:

think austerity; US: think growth) suggest that the euro should

outperform the U.S. dollar over the long term, assuming the

not-so-negligible scenario of a more severe fallout from the Eurozone

debt crisis won’t materialize.

It may help to keep in mind that historically

inflation is the response to a deflationary shock. If market forces were

left to themselves, we believe the credit bust of 2008 would have

caused a major deflationary shock. It’s the reaction of policy makers

that fight market forces that may lead to inflation. Bernanke as of late

brushed off such pessimism. As the charts above show, however, gold has

been a sensitive – and sensible I might add - indicator to the

trigger-friendliness of our central bankers.

No comments:

Post a Comment